Captive insurance, often referred to as the best-kept secret in the insurance industry, has been gaining traction in recent years. It offers businesses a chance to take control of their risks and potentially reap substantial financial benefits. One particular aspect of captive insurance, known as 831(b) captives, has sparked significant interest due to the potential tax advantages it offers under the IRS 831(b) tax code. These microcaptives provide an opportunity for small to mid-sized businesses to create their own insurance company, tailor-made to their unique needs.

So, what exactly is captive insurance? Simply put, it is a form of self-insurance where a business creates its own insurance company to cover its own risks. Rather than relying on traditional insurance companies, who often dictate terms and premiums, captive insurance allows a business to have more control over their coverage, while potentially saving costs in the process. It can be seen as an alternative risk management strategy, allowing businesses to better manage their exposure to risks and protect against unexpected losses.

One key advantage of captive insurance is the potential tax benefits it can provide. Under the aforementioned IRS 831(b) tax code, qualifying small captives can elect to be taxed only on their investment income, rather than on their underwriting income. This can result in substantial tax savings for businesses, as they are able to retain more of their premiums and investment earnings within the captive. It’s important to note, however, that captives must meet certain criteria and adhere to specific regulations to qualify for these tax advantages.

In the next sections, we will delve deeper into the intricacies of captive insurance, exploring its benefits, potential risks, and the process of establishing and operating a captive insurance company. Brace yourself for an eye-opening journey into the world of captive insurance, as we unravel its mysteries and guide you towards unlocking its full potential.

What is Captive Insurance?

Captive insurance is a unique form of self-insurance that allows companies to customize their insurance coverage according to their specific needs. Unlike traditional insurance, where businesses pay premiums to an external insurance company, captive insurance allows businesses to create their own insurance company to cover the risks associated with their operations.

Captive insurance companies, also known as captives, are established by businesses to provide coverage for their own risks. By forming a captive insurance company, businesses can retain more control over their insurance policies, claims administration, and investment strategies. This alternative risk management tool offers businesses the opportunity to obtain coverage that may be unavailable or too expensive in the traditional insurance market.

One type of captive insurance company that has gained popularity is the microcaptive, particularly those established under Section 831(b) of the IRS tax code. Under this code, certain small insurance companies can elect to be taxed only on their investment income, allowing them to benefit from potential tax advantages. Microcaptives can be an attractive option for businesses that qualify under the IRS guidelines and seek to optimize their risk management and tax planning strategies.

In summary, captive insurance provides businesses with the ability to tailor insurance coverage to their specific needs and gain more control over their risk management strategies. Microcaptives, under IRS Section 831(b), offer potential tax advantages for qualifying businesses. By understanding and demystifying captive insurance, companies can unlock its benefits and achieve more customized and cost-effective insurance solutions.

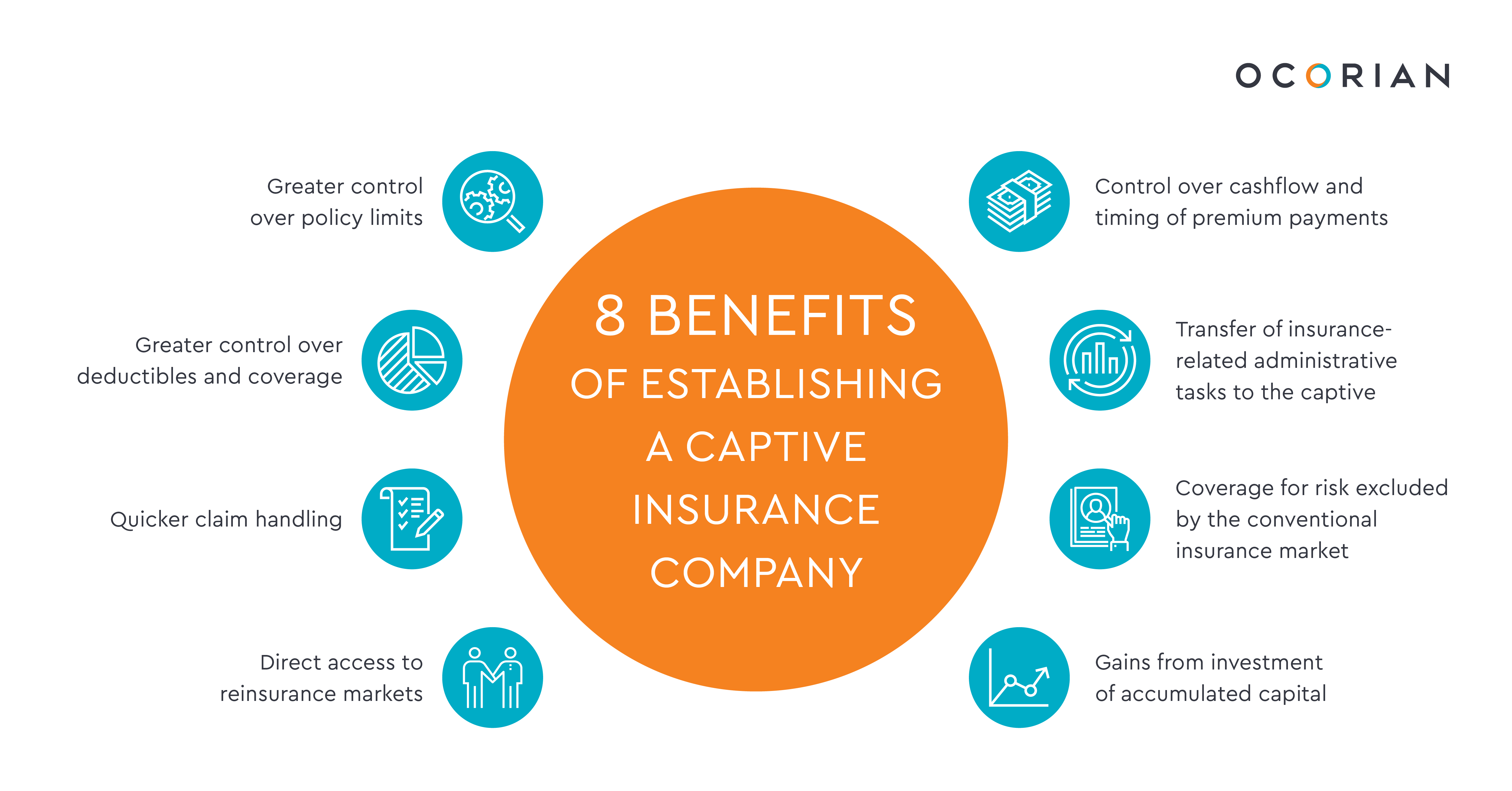

The Benefits of Captive Insurance

Captive Insurance, also known as 831b or microcaptive insurance, offers a range of benefits that can significantly impact businesses. Let’s explore some of the advantages of this unique form of insurance.

Firstly, captive insurance allows businesses to have more control over their insurance coverage. By forming a captive insurance company, businesses can create a tailored insurance program that aligns specifically with their needs and risk profile. This means they can include coverage for risks that traditional insurance policies may not cover, providing a higher level of protection.

Secondly, captive insurance offers potential financial advantages. Under the IRS 831(b) tax code, captive insurance companies can qualify for certain tax benefits. By electing to be treated as a small insurance company, captives can benefit from reduced tax rates on their premium income. This can lead to substantial tax savings for the business.

Lastly, captive insurance can promote better risk management practices. By having a captive insurance program, businesses are incentivized to take a more proactive approach towards risk management. They have a direct stake in managing and reducing their risks, as any losses paid out by the captive come out of their own funds. This encourages businesses to implement stronger risk mitigation strategies and improve overall risk culture.

In conclusion, captive insurance offers businesses increased control over their insurance coverage, potential tax savings, and promotes better risk management practices. These benefits make captive insurance an appealing option for organizations looking to better align their insurance programs with their unique needs and risk profile.

Understanding the IRS 831(b) Tax Code

The IRS 831(b) tax code refers to a specific section within the tax legislation that governs captive insurance companies. Captive insurance, as an alternative risk management strategy, has gained significant attention in recent years. It enables businesses to establish their own insurance company to cover the risks faced by their operations, subsidiaries, or affiliated entities.

Under the IRS 831(b) tax code, captive insurance companies that qualify as microcaptives can elect to be taxed on their underwriting profits at a reduced rate. Microcaptives are those with annual written premiums that do not exceed $2.3 million. By choosing this tax election, these small captive insurance companies can potentially benefit from tax advantages, allowing them to retain more of their underwriting profits.

However, it is important to note that the IRS has issued guidelines and regulations to prevent abusive practices surrounding captive insurance arrangements. Captive insurance companies must meet certain criteria, such as necessary risk distribution and adequate annual premium levels, to qualify for the tax benefits outlined in the 831(b) tax code. Failure to comply with these regulations can result in penalties and the disqualification of the tax election.

In summary, the 831(b) tax code provides an avenue for small captive insurance companies, known as microcaptives, to benefit from reduced taxation on underwriting profits. However, adherence to the guidelines and regulations set forth by the IRS is crucial to ensure compliance and avoid potential penalties.